Links:https://www.trendforce.com/presscenter/news/20200514-10309.h ...

Q1' 2020 Global Top 10 OSAT Ranking

Packaging and Testing Industry Grows in 1Q20 Despite Seasonality, with Daunting Challenges Ahead in 2H20, Says TrendForce

Packaging and Testing Industry Grows in 1Q20 Despite Seasonality, with Daunting Challenges Ahead in 2H20, Says TrendForce

14 May 2020, Semiconductors, John Wang

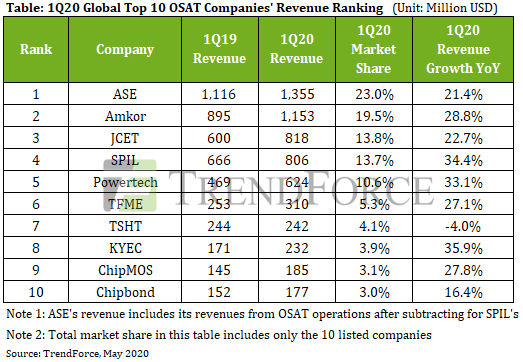

According to TrendForce’s latest investigations, owing to the gradual easing of the China-U.S. trade war and increased packaging and testing demand for 5G, AI chips, and smartphones, the global packaging and testing (OSAT, outsourced semiconductor assembly and test) industry was able to sustain the upward trend of its quarterly revenue in 1Q20. The global top 10 OSAT companies’ revenues combined for US$5.903 billion in 1Q20, a 25.3% increase YoY. However, as the demand of end devices came to a screeching halt because of the COVID-19 pandemic, the OSAT industry may potentially start to decline in 2H20.

TrendForce indicates that OSAT industry leader ASE posted 1Q20 revenue of $1.355 billion, a 21.4% increase YoY, thanks primarily to packaging demand for applications including 5G smartphone AiP (Antenna in Package) and other consumer electronics. Second-place Amkor similarly benefitted from strong demand from 5G communications and consumer electronics, reaching $1.153 billion in 1Q20 revenue, a 28.8% increase YoY. SPIL also profited from the increase in demand from the two aforementioned applications and registered 1Q20 revenue of $806 million, a 34.4% increase YoY. The magnitude of SPIL’s revenue growth was more noticeable relative to those of most other OSAT companies. Although SPIL maintained its fourth-ranked position on the list, the company is progressively closing in on third-ranked JCET.

The overall revenue growth of the three dominant Chinese OSAT companies in 1Q20 can be mostly attributed to the gradual stabilization of China-U.S. relations. Notably, TSHT is the only company on the top 10 list to undergo a YoY decline in revenue. TrendForce believes TSHT’s decline occurred because the company had to push back its packaging schedule for consumer electronics, in favor of fulfilling packaging orders placed by the Chinese government during the onset of COVID-19 for disease-prevention applications such as IR sensor components.

OSAT giant Powertech, which specializes in memory product packaging and testing, saw its revenue growing by 33.1% YoY in 1Q20, due to orders placed by Kingston, Micron, and Intel. Testing supplier KYEC posted the most remarkable growth out of the top 10 in 1Q20 because of surging orders for 5G smartphones, base station chips, CMOS image sensors, and server chips. Its revenue grew by 35.9% YoY. Also worth mentioning is that display panel driver IC and memory product packaging specialist ChipMOS joined the top 10 by leapfrogging from 11th place in 2019 to 9th place this year. Its performance took place due to increased demand for memory products, large-sized display driver IC (LDDI), and touch and display driver IC (TDDI).

The gradual deceleration of the China-U.S. trade war starting in 3Q19 was, on the whole, beneficial to the global OSAT industry’s performance in 1Q20. Most of the companies in the top 10 were able to maintain their growth momentum even during the traditionally weak first quarter. Now that the pandemic has significantly reduced the demand for end devices, a similar situation is likely to take place in the OSAT industry in 2Q20, however. Furthermore, as tensions mount once again between China and the U.S., TrendForce expects the OSAT industry to face immense market challenges in 2H20.

According to TrendForce’s latest investigations, owing to the gradual easing of the China-U.S. trade war and increased packaging and testing demand for 5G, AI chips, and smartphones, the global packaging and testing (OSAT, outsourced semiconductor assembly and test) industry was able to sustain the upward trend of its quarterly revenue in 1Q20. The global top 10 OSAT companies’ revenues combined for US$5.903 billion in 1Q20, a 25.3% increase YoY. However, as the demand of end devices came to a screeching halt because of the COVID-19 pandemic, the OSAT industry may potentially start to decline in 2H20.

TrendForce indicates that OSAT industry leader ASE posted 1Q20 revenue of $1.355 billion, a 21.4% increase YoY, thanks primarily to packaging demand for applications including 5G smartphone AiP (Antenna in Package) and other consumer electronics. Second-place Amkor similarly benefitted from strong demand from 5G communications and consumer electronics, reaching $1.153 billion in 1Q20 revenue, a 28.8% increase YoY. SPIL also profited from the increase in demand from the two aforementioned applications and registered 1Q20 revenue of $806 million, a 34.4% increase YoY. The magnitude of SPIL’s revenue growth was more noticeable relative to those of most other OSAT companies. Although SPIL maintained its fourth-ranked position on the list, the company is progressively closing in on third-ranked JCET.

The overall revenue growth of the three dominant Chinese OSAT companies in 1Q20 can be mostly attributed to the gradual stabilization of China-U.S. relations. Notably, TSHT is the only company on the top 10 list to undergo a YoY decline in revenue. TrendForce believes TSHT’s decline occurred because the company had to push back its packaging schedule for consumer electronics, in favor of fulfilling packaging orders placed by the Chinese government during the onset of COVID-19 for disease-prevention applications such as IR sensor components.

OSAT giant Powertech, which specializes in memory product packaging and testing, saw its revenue growing by 33.1% YoY in 1Q20, due to orders placed by Kingston, Micron, and Intel. Testing supplier KYEC posted the most remarkable growth out of the top 10 in 1Q20 because of surging orders for 5G smartphones, base station chips, CMOS image sensors, and server chips. Its revenue grew by 35.9% YoY. Also worth mentioning is that display panel driver IC and memory product packaging specialist ChipMOS joined the top 10 by leapfrogging from 11th place in 2019 to 9th place this year. Its performance took place due to increased demand for memory products, large-sized display driver IC (LDDI), and touch and display driver IC (TDDI).

The gradual deceleration of the China-U.S. trade war starting in 3Q19 was, on the whole, beneficial to the global OSAT industry’s performance in 1Q20. Most of the companies in the top 10 were able to maintain their growth momentum even during the traditionally weak first quarter. Now that the pandemic has significantly reduced the demand for end devices, a similar situation is likely to take place in the OSAT industry in 2Q20, however. Furthermore, as tensions mount once again between China and the U.S., TrendForce expects the OSAT industry to face immense market challenges in 2H20.